"Someone is sitting in the shade today because someone planted a tree a long time ago." - Warren Buffett

Many people spend their careers focused on reaching the next salary milestone or securing a promotion, but financial progress shouldn't be measured by your paycheck alone. The decisions you make in your peak earning years are just as important as the size of your paycheck. One of the most significant risks is lifestyle creep, which is the tendency for everyday spending to rise alongside income. How you manage a salary raise today can have a significant impact on your long-term financial security. Without a strategy for handling salary increases, even a high-earning household can find itself ill-prepared for the future.

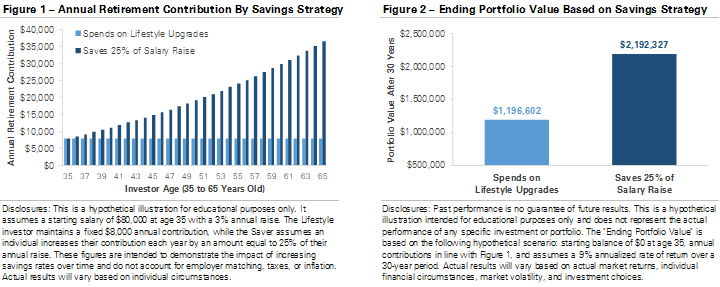

The charts below demonstrate how different approaches to a salary increase can impact a retirement portfolio’s growth. They’re based on a hypothetical scenario: two individuals aged 35 make $80,000 annually and receive 3% annual raises. Both start by contributing 10% of their salary, or $8,000, to retirement savings. The two sets of bars in Figure 1 track different strategies for managing the raises and retirement contributions. The Lifestyle individual keeps their annual contribution fixed at $8,000. Every dollar of every raise is spent on immediate lifestyle upgrades, such as a nicer car, another trip, or higher discretionary spending. The Saver individual takes a more balanced approach, setting aside 25% of every raise while enjoying the rest. For example, a $2,000 raise would increase the next year’s contribution by $500, or 25%.

While both individuals earn the same amount, their retirement savings quickly diverge. Figure 2 graphs the ending portfolio values at age 65, reflecting 30 years of each individual’s savings strategy. These hypothetical ending account values assume the portfolios earn a +9% annual return. Over 30 years, the Lifestyle individual contributed nearly $250,000, which grew to nearly $1.2 million. The Saver individual contributed nearly $630,000, which grew to nearly $2.2 million, almost $1,00,000 larger than their peer’s. The difference isn’t just additional savings but decades of compounding that can extend a portfolio’s life in retirement or create the option to retire earlier. In contrast, the Lifestyle individual not only saves less but also increases their base cost of living, which will require a larger portfolio to sustain their lifestyle in retirement.

Building long-term wealth isn’t just about what you earn; it’s about how you manage the surplus as you earn it. Raises can either disappear into lifestyle upgrades or become a powerful tool for future security and flexibility. It’s about finding a balance between enjoying the reward of hard work today and saving for your future. There’s no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Everyone’s retirement looks different, and the right strategy depends on your goals and life stage. Our goal is to help you create a savings strategy tailored to your unique needs and goals so that when the time comes, you’re ready to enjoy retirement.

IMPORTANT DISCLOSURES

Clare Market Investments, LLC is a registered investment advisor. This material is for informational purposes only. It is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a recommendation to buy a security. The information is derived from sources believed to be reliable and accurate as of the date of this report, but Clare Market has not audited this information to validate accuracy. Further, information may be at a point in time and subject to change. This summary is based exclusively on an analysis of general market conditions and does not speak to the suitability of any specific proposed securities transaction or investment strategy. Judgments or recommendations found in this report may differ materially from what may be presented in a long-term investment plan and are subject to change at any time. This report’s authors will not advise you as to any changes in figures or views found in this report. Investors should consult with their investment advisor to determine the appropriate investment strategy and investment vehicle. Investment decisions should be made based on the investor’s specific financial needs and objectives, goals, time horizon, and risk tolerance. Except for the historical information contained in this report, certain matters are forward-looking statements or projections that are dependent upon risks and uncertainties, including but not limited to such factors and considerations such as general market volatility, global economic risk, geopolitical risk, currency risk and other country-specific factors, fiscal and monetary policy, the level of interest rates, security-specific risks, and historical market segment or sector performance relationships as they relate to the business and economic cycle. See claremarket.com for additional information and disclosures. © 2026 Clare Market Investments, LLC. All Rights Reserved.